- January 30, 2020

- Posted by: Vincent Sarullo

- Category: Direct Lending, Fund Administration, Fund of Funds, Hedge Funds, Private Equity / Venture Capital, Real Estate, Tax Liens

Tower Fund Services have been around for a while and can guide firms and fund managers in the right direction. For example, from a legal formation perspective, a hedge fund and a private equity fund are the same type of entities; typically, a limited partnership and on an occasion an LLC. The legal form doesn’t determine the type of fund, how the fund is operated does. Fees, liquidity and investor capital terms drive the distinction. Enjoy the guide to alternative investment funds.

Limited Partnership

Alternative investment funds formed in the US are primarily invested in by high net worth individuals and are formed as limited partnerships. Partnerships are pass-through entities and are not taxable entities themselves. The structure’s pass-through characteristics enable the investors to get the attributes of the fund performance passed through to them for tax purposes. The interest, dividends, short-term and long-term capital gains, along with the fund expenses, are directly picked up on the investor’s personal tax returns. The general partner of a domestic limited partnership receives a profit allocation or carried interest in the profits it generates for its investors. In essence, the percentage the general partner earns in profits is re-allocated away from the limited partners’ (investors’) accounts and to the general partner’s capital account. The general partner then enjoys the same tax benefits from the characteristics of income and expenses.

Limited Liability Company

A less-frequently utilized legal structure for funds is the limited liability company (LLC). It is almost identical to the limited partnership in all practical senses, but it does not have limited partners and a general partner. Instead, it has members and a managing member.The LLC structure is most commonly used for the fund’s management company and general partner entities.

Offshore Funds (Corporations)

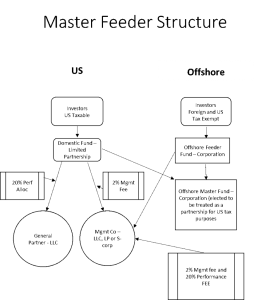

US fund managers who are tax-exempt (IRAs and other pension plans) and foreign investors will set up a master-feeder or mini-Master fund structure (see below). A traditional master-feeder fund structure will encompass three separate entities: a master fund, an offshore feeder fund, and an onshore feeder fund. The master and offshore feeder funds are domiciled in an offshore jurisdiction (Cayman Islands, BVI, Bermuda, etc.) and the onshore feeder is set up in the US (Delaware, etc.). The master fund has only two investors, the onshore and offshore feeder funds. The investors in the fund will invest their money through either of the feeder funds and the capital invested is then transferred (invested) into the master fund, where all the trading activity will occur.

Master Feed Structure

Master Feed Structure

The performance of the master fund is then allocated between the two feeder funds, based on the relative ownership percentages the feeder funds have in the master. That performance is then captured by the feeder funds and allocated among the investors in those feeders. In order to retain the US tax attributes of the investment activity, the master fund will typically make a “check the box” election with the IRS to be treated as a partnership for US tax purposes.

Next week, we will take a look at separately managed accounts and the challenges that may arise with managers handling several accounts, as well as alternatives for large investors.